Personal finance is not just about how much you earn—it’s about how you behave with your money.

Even if someone earns a high salary, they can still struggle financially if their spending habits are poor. On the other hand, someone with a modest income can achieve financial stability through wise behavior and self-discipline.

In this blog, you’ll learn why is personal finance dependent upon your behavior, behavioral factors that impact financial decisions, and more.

What Is Personal Finance Behavior?

Personal finance behavior refers to the choices and habits you develop around earning, spending, saving, borrowing, and investing money.

You might have heard this before:

“It’s not how much you make, it’s how you manage it.”

That’s because behavior controls what happens to your money after you receive it. Good behavior helps you grow wealth. Bad behavior leads to debt and stress.

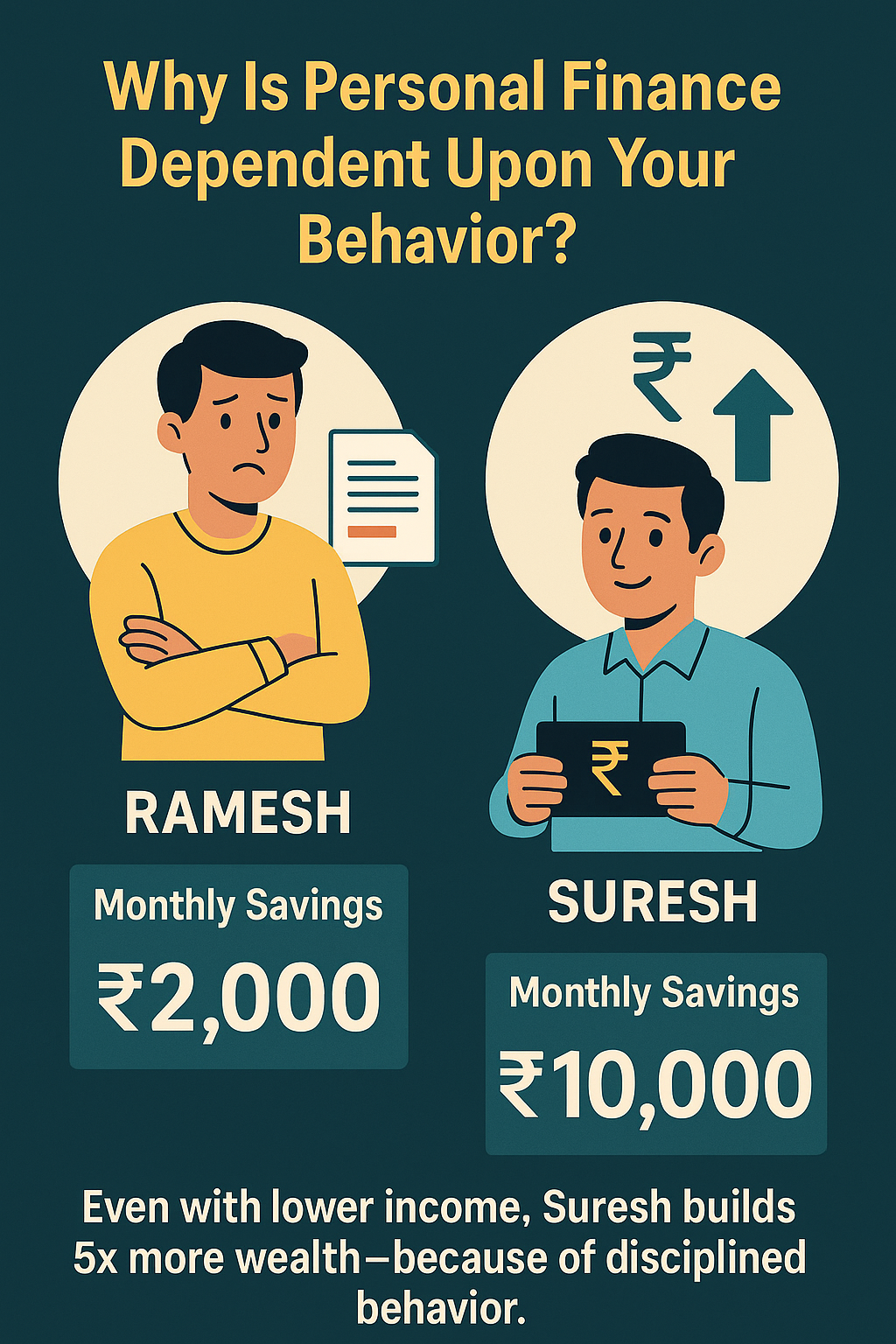

Real-Life Example: The Power of Behavior Over Income

Let’s compare two individuals:

| Person | Monthly Income | Monthly Expenses | Monthly Savings | Savings After 1 Year |

| Ramesh | ₹60,000 | ₹58,000 | ₹2,000 | ₹24,000 |

| Suresh | ₹40,000 | ₹30,000 | ₹10,000 | ₹1,20,000 |

Even though Ramesh earns more, Suresh saves 5x more in one year because of better behavior.

Now let’s take it further…

5-Year Wealth Growth: A Calculated Example

Let’s say Suresh continues saving ₹10,000/month and invests it in a mutual fund with an average return of 10% per year.

We’ll use a SIP calculator to find his returns.

Monthly SIP = ₹10,000

Tenure = 5 years

Expected Annual Return = 10%

👉 Final Value ≈ ₹7,75,000

👉 Invested Amount = ₹6,00,000

👉 Interest Earned = ₹1,75,000

In contrast, Ramesh, saving only ₹2,000/month:

Monthly SIP = ₹2,000

Tenure = 5 years

Expected Annual Return = 10%

👉 Final Value ≈ ₹1,55,000

👉 Invested Amount = ₹1,20,000

👉 Interest Earned = ₹35,000

Conclusion: Even with lower income, Suresh builds 5x more wealth—because of disciplined behavior.

Why Is Personal Finance Dependent Upon Your Behavior?

Here are the key reasons:

1. Knowledge Alone Isn’t Enough

Most people know they should save money, avoid debt, and invest—but they don’t act on it.

📌 Reason: Lack of self-control, habits, or emotional triggers.

2. Money Is Emotional

Many financial decisions are based on feelings like fear, stress, or peer pressure.

Example:

- Buying expensive phones to impress others.

- Selling investments too early due to market panic.

3. Delayed Gratification Builds Wealth

People who can wait for long-term rewards instead of instant joy tend to save and invest more.

Example: Investing ₹500 today can become ₹1,300 in 10 years (at 10% annual return).

Common Behavioral Patterns in Personal Finance

| Behavior | Effect on Finance |

| Impulsive Shopping | Reduces savings, increases credit card debt |

| Ignoring Budgeting | Leads to overspending |

| Fear of Investing | Misses growth opportunities |

| Emotional Lending | Lending to friends/family without planning |

| Living Paycheck to Paycheck | Zero long-term security |

Behavioral Economics: Why We Make Bad Money Decisions

Behavioral economics explains how psychological factors affect money decisions.

Key concepts

- Loss Aversion: Fear of losing makes people avoid investing.

- Present Bias: Preferring spending now instead of saving for later.

- Anchoring: Making decisions based on the first number you see (even if irrelevant).

📌 Example: A person refuses to buy a quality item for ₹1,200 just because they saw a cheaper one for ₹999 earlier—even if the expensive one lasts longer.

How to Change Financial Behavior for Better Results

1. Track Your Spending

Write down everything you spend for one month. You’ll be shocked at where the money goes.

2. Use the 50/30/20 Rule

- 50% needs (rent, food)

- 30% wants (shopping, movies)

- 20% savings/investments

3. Set Smart Goals

| Goal Type | Example |

| Short-Term Goal | Save ₹20,000 for a vacation |

| Medium-Term Goal | Build ₹2 lakh emergency fund |

| Long-Term Goal | Invest ₹1 crore for retirement |

4. Automate Savings

Make saving a habit, not a choice. Auto-debit a portion of your income on payday.

5. Limit Emotional Spending

Wait 24 hours before making large purchases. Ask:

Do I need this or just want it?

Mini Calculation: Impact of Daily Saving Habit

If you save just ₹100 per day, here’s what you get:

| Time Period | Total Savings | At 8% Interest (FD or SIP) |

| 1 Year | ₹36,500 | ₹38,900 |

| 5 Years | ₹1,82,500 | ₹2,23,800 |

| 10 Years | ₹3,65,000 | ₹5,49,000 |

👉 Daily behavior = Long-term results.

Bad Habits That Kill Financial Growth

| Habit | Long-Term Effect |

| Not paying credit card on time | Penalties, bad credit score |

| Spending more than you earn | Debt trap |

| No emergency fund | Borrowing during emergencies |

| No insurance | High risk during accidents/illness |

| Ignoring financial education | Poor decisions |

Positive Financial Behaviors to Practice Daily

- Track your expenses

- Stick to a budget

- Save first, spend later

- Invest monthly (even small amounts)

- Avoid impulse purchases

- Review your goals every month

Quotes That Reinforce This Lesson

“Successful investing is about behavior, not brains.” – Carl Richards

“You manage money best when you manage yourself better.”

Conclusion: Control Your Behavior, Control Your Finances

Your income can help you survive, but your behavior helps you thrive. Good financial behavior builds wealth, peace of mind, and a secure future. You don’t need to be a finance expert—just be consistent, disciplined, and smart with your money.

👉 Remember, financial success is 80% behavior, 20% knowledge.