Financing a car is one of the most common ways to buy a vehicle today. But if you’re new to the process, it can seem confusing—what does it really mean to “finance” a car? What are interest rates, down payments, and loan terms? How do you avoid paying too much? How to finance a car?

In this blog, you’ll learn everything about car financing, with step-by-step help, examples, and easy calculations—so you can drive away confidently!

What Does It Mean to Finance a Car?

Financing a car means borrowing money (usually from a bank, dealership, or credit union) to pay for the car, and repaying it over time with interest.

You’re not paying the full cost upfront. Instead:

- You make a down payment (some money at the start)

- You borrow the rest as a loan

- You pay monthly installments over a fixed period (called a loan term)

Example of Car Financing

Let’s say you want to buy a car that costs ₹10,00,000 (or $12,000).

| Component | Amount |

| Car Price | ₹10,00,000 |

| Down Payment (20%) | ₹2,00,000 |

| Loan Amount Needed | ₹8,00,000 |

| Interest Rate (10%) | 10% per annum |

| Loan Term | 5 years (60 months) |

You borrow ₹8,00,000 for 5 years at 10% interest.

Monthly EMI Calculation (Using Flat Rate Method):

EMI = (Loan + Interest) / Number of Months

Interest = ₹8,00,000 × 10% × 5 = ₹4,00,000

Total repayment = ₹8,00,000 + ₹4,00,000 = ₹12,00,000

EMI = ₹12,00,000 / 60 = ₹20,000 per month

✅ So, you’ll pay ₹20,000 every month for 5 years.

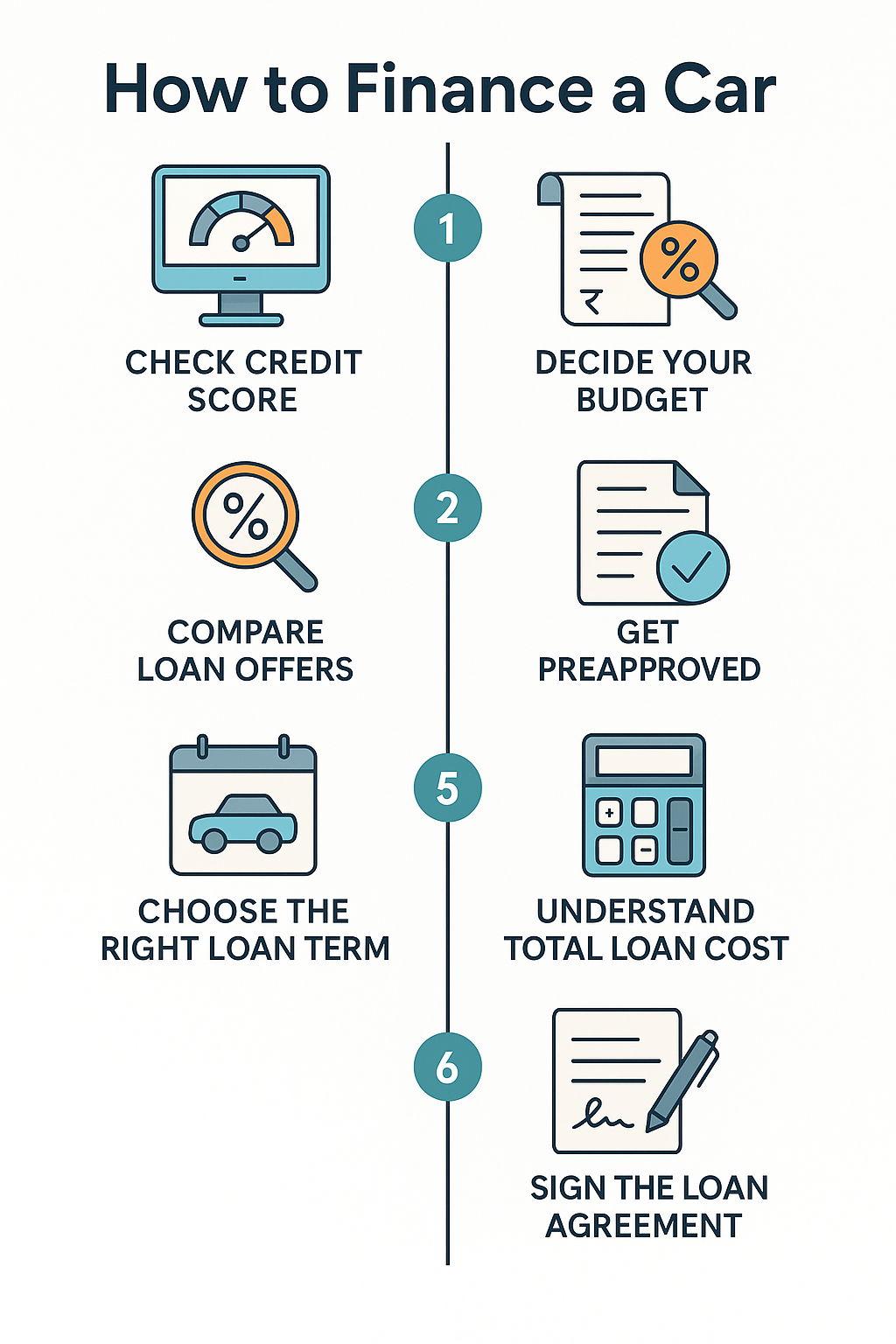

Step-by-Step: How to Finance a Car

Let’s break down the car financing process based on best practices:

1. Check Your Credit Score

Your credit score affects:

- Interest rate offered

- Loan approval chances

- Down payment requirements

🔹 Tip: A score above 750 is considered excellent in India; above 700 is good in the U.S.

2. Decide Your Budget

Use the 20/4/10 Rule:

- Pay 20% down payment

- Take a loan of max 4 years

- Monthly payments should be less than 10% of your monthly income

📌 If you earn ₹50,000/month → EMI should be ≤ ₹5,000.

3. Compare Loan Offers

From:

- Banks (like Bank of America)

- Online Lenders (like NerdWallet’s partners)

- Dealerships (may offer special deals or zero-interest)

Check:

- Interest rates

- Processing fees

- Prepayment penalties

4. Get Pre Approved (If Possible)

Getting pre approved means the lender checks your eligibility before car shopping—this:

- Gives you a clear budget

- Helps you negotiate better with dealers

- Speeds up final paperwork

5. Choose the Right Loan Term

Longer terms = lower EMIs but more total interest

Shorter terms = higher EMIs but save on interest

| Term | EMI (approx) | Total Interest (at 10%) |

| 3 Years | ₹26,667 | ₹1,60,000 |

| 5 Years | ₹20,000 | ₹4,00,000 |

| 7 Years | ₹15,238 | ₹5,68,000 |

6. Understand Total Loan Cost

Always calculate:

- Total repayment amount

- Interest paid over time

- Processing charges

Use an auto loan calculator (like Bank of America’s or NerdWallet’s) to experiment with values.

7. Sign the Loan Agreement

Before signing:

- Read terms carefully

- Check EMI start date

- Look for prepayment and foreclosure clauses

Then, drive your car home! 🎉

Tips to Save Money While Financing a Car

- Improve your credit score before applying

- Negotiate the car price before talking about financing

- Choose used cars to reduce loan amount

- Avoid unnecessary add-ons (like extended warranties)

- Prepay when possible to reduce interest burden

Bank vs Dealership Financing: Which is Better?

| Feature | Bank Financing | Dealership Financing |

| Interest Rates | Usually lower (esp. for good credit) | May offer 0% or higher rates |

| Transparency | More transparent, standard offers | May include hidden fees |

| Convenience | Slightly slower process | Faster if buying directly |

✅ According to Experian, dealership financing is faster but banks offer better long-term value.

What Affects Your Car Loan Interest Rate?

- Credit score

- Loan term (longer = higher rates)

- Down payment (higher down = lower rate)

- New vs Used car (new = lower rates)

- Lender policies

Loan Calculator Table (Interest Breakdown)

Here’s a simple table showing how your interest varies with the loan term:

| Loan Amount | Interest Rate | Term | Monthly EMI | Total Interest Paid |

| ₹8,00,000 | 10% | 3 yr | ₹26,667 | ₹1,60,000 |

| ₹8,00,000 | 10% | 5 yr | ₹20,000 | ₹4,00,000 |

| ₹8,00,000 | 10% | 7 yr | ₹15,238 | ₹5,68,000 |

Summary: Key Takeaways

- Financing a car helps you buy it now and pay in parts

- You need to check your credit score, budget, and compare offers

- Always calculate total cost, not just EMI

- Shorter loan = less interest

- Use loan calculators to plan better

Conclusion

Buying a car is exciting, and financing makes it easier for many people. But smart financing starts with understanding your loan options, doing the math, and avoiding long-term traps.

Always remember: the best deal is not the lowest EMI, but the lowest total cost.